Last Updated on 13/07/2026 by Damin Murdock and Malak Amgad

Offshore staffing and outsourcing are no longer exceptions in Australia. Since COVID, Australian businesses have increasingly relied on remote offshore workers. These workers no longer exclusively perform administrative tasks, but are now handling core functions such as marketing, customer service, bookkeeping and other operational functions.

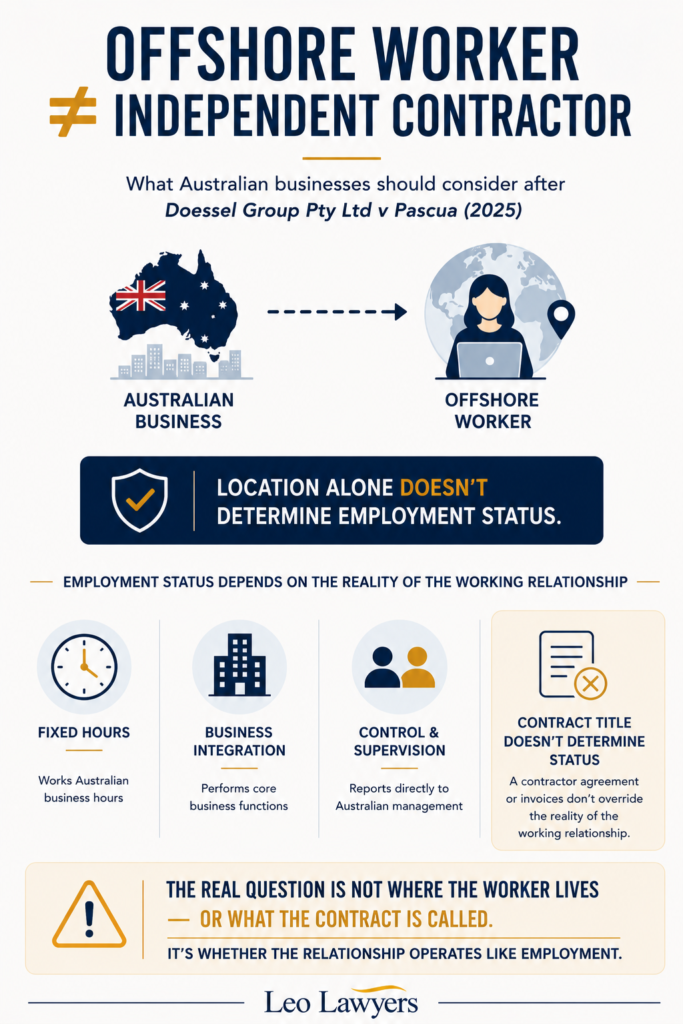

Consequently, businesses have assumed that since these workers live overseas, pay taxes in their home country, perform all work remotely, and are engaged as private contractors, Australian employment laws don’t apply.

That is, until the February 2025 Fair Work Commission decision in Doessel Group Pty Ltd v Pascua cast doubt on these assumptions. The case concerns a legal assistant based in the Philippines, who worked remotely for an Australian law practice. She was engaged under an independent contractor arrangement. When the relationship ended, the worker commenced unfair dismissal proceedings in the Fair Work Commission.

In our view, even though the worker succeeded in its unfair dismissal claims, the significance of the decision lies in the Commission’s willingness to entertain the possibility that a completely remote offshore worker could be considered an employee under Australian employment laws. This directly impacts businesses that have built completely offshore teams. The question is if neither geography nor the contract terms determines the workers’ status, what does?

Pascua may be less about offshore workers and more about the changing approach to contractor relationships.

Most of the commentary surrounding the decision focuses on the worker’s location. However, that may be the least important detail of the dispute.

The FWC’s reasoning is reflective of a trend that recently emerged in Australian employment law. Courts and tribunals examine the substance and nature of the working relationship rather than the labels or the contract nomenclature that the parties apply to them.

Viewed through that lens, the Pascua decision is just another chapter in the debate around contractor classification. From the High Court’s decisions in Personnel Contracting and Jamsek to the Federal Government’s Closing Loopholes reforms and disputes involving gig economy workers, courts and lawmakers are focusing more and more on the boundary between genuine contracting and employment.

The worker was engaged to perform legal support for an Australian law practice. Within 12 months of her employment, she was training others. The Commission considered the degree of her involvement in the business and whether the work relationship bore the hallmarks of employment. That analysis is not new to those who have followed recent developments concerning contractor misclassification.

What makes Pascua different is that those questions are asked regarding a worker who has no ties to Australia.

The most interesting part of Pascua is what it leaves unresolved

Perhaps the most important aspect of Pascua is not what the Commission decided, but what it did not decide.

The Commission did not determine that all offshore workers are covered by Australian employment law. Nor did it decide whether superannuation is due for offshore workers. It didn’t decide whether PAYG withholding obligations arise as a result of this employment classification, nor how these obligations would be fulfilled given the workers’ offshore status. Neither did it touch on how Australian workplace laws interact with labour laws in the workers’ home countries.

Moreover, discussions around the decision focus on unfair dismissal because that was the claim. However, unfair dismissal may be only the beginning of the conversation.

If an offshore worker is considered an employee, a range of secondary issues may arise. These include minimum employment standards, leave entitlements, and many more.

This is where the decision becomes commercially significant.

Many offshore workers operate in arrangements that resemble employment. They work fixed hours, report to their managers directly, perform core operational functions, and work full-time. The only obvious distinction is that they live in another country and submit invoices instead of timesheets.

The FWC has decided that geography alone should not determine the legal classification of workers,

The real issue is not the invoice

There is a practical irony in many offshore staffing arrangements.

Businesses are aware that contractor labels are not legally determinative. Yet continue to structure offshore arrangements on the assumption that a contractor agreement, or invoicing terms and an overseas address will be enough.

A worker can have a contractor agreement, submit their own invoices rather than getting a salary, and still be considered an employee in substance. This risk increases when the worker works fixed Australian business hours, reports to Australian management and performs work personally rather than operating an independent business that offers these services.

Many offshore workers occupy a middle ground that the law does not deal with very well. They are not considered traditional employees, but they are also not traditional independent business contractors. Future disputes are likely to arise regarding these grey areas and unanswered questions.

Superannuation remains an unresolved risk.

One of the most important unanswered questions is superannuation.

Australian superannuation law can treat some contractors as employees for superannuation guarantee purposes, particularly where they are engaged mainly for their labour and perform the work personally.

That does not mean Pascua decided that superannuation must be paid to offshore workers. It did not.

However, the decision may encourage closer scrutiny of offshore arrangements where the worker performs personal labour for one Australian business.

The fact that a worker lives overseas or invoices hourly should not be treated as the end of the analysis. The proper question is whether the arrangement, in substance, creates an obligation under the relevant employment, tax or superannuation legislation.

For many businesses, that question has never been properly assessed.

PAYG withholding should not be confused with employment status

The tax position is also more nuanced than some commentary suggests.

A finding that a worker may be an employee for one legal purpose does not automatically mean that Australian PAYG withholding obligations apply.

Where a worker is a foreign resident, performs all work overseas and has no Australian tax file number, the PAYG analysis requires separate consideration of tax residency, source of income, double tax agreements and the specific statutory withholding rules.

In other words, employment law and tax law do not always move together.

This is why businesses should be careful not to draw overly broad conclusions from Pascua. The decision may increase employment law risk, but it does not by itself answer every tax and payroll question.

The likely legacy of Pascua

It is unlikely that Pascua will be remembered as a case that completely rewrote the law for offshore workers.Its likely significance is more subtle.

The decision may make it harder for Australian businesses to rely solely on overseas location as a defence to employment-related claims. It may also encourage workers, advisers and regulators to scrutinise offshore contractor arrangements more closely.

That does not mean businesses need to stop using offshore contractors. Many offshore contractor arrangements remain legitimate.

However, businesses should be honest about the nature of the relationship. If a worker is engaged indefinitely, works fixed hours, performs core business functions and operates under close supervision, the arrangement may carry more legal risk than the contract suggests.

The practical takeaway for Australian businesses

The lesson from Pascua is not that every offshore worker is an employee.

The stronger lesson is that Australian businesses should review whether their offshore staffing arrangements genuinely operate as independent contractor arrangements.

Contractor agreements, invoices and overseas location are relevant, but they may not be enough if the day-to-day reality points in a different direction.

For businesses that rely heavily on offshore staff, the safest approach is to assess the arrangement before a dispute arises. Once the relationship breaks down, the legal analysis often becomes more difficult, more expensive and more commercially disruptive.

Need expert legal advice? feel free to contact Damin Murdock at Leo Lawyers via our website, on (02) 8201 0051 or at office@leolawyers.com.au. Further, if you liked this article, please subscribe to our newsletter via our Website, and subscribe to our YouTube, LinkedIn, Facebook and Instagram. If you liked this article or video, please also give us a favorable Google review.

DISCLAIMER: This article is not to be taken as legal advice and is general in nature. If you require specific advice, please contact us.

Damin Murdock (J.D | LL.M | BACS - Finance) has over 17 years of experience as a commercial lawyer. He helps businesses navigate construction and technology law. Damin has held several big leadership roles, including serving as a director of a national law firm and the Chief Legal Officer for Lawpath.

He has personally helped more than 2,000 startups and small businesses. With over 300 five-star reviews, his clients clearly value his practical advice and simple way of explaining things. Damin has also hosted over 100 webinars that thousands of people have watched to get reliable legal help.